Hp 17bII+ Financial Calculator

Edition June January

Printing History

Welcome to the hp17bII+

Welcome to the hp 17bII+

Contents

Using Parentheses in Calculations

Error Messages

Power Function Exponentiation

Saving and Reusing Numbers

Time Value of Money

Interest Rate Conversions

Cash Flow Calculations

Depreciation

Bonds

10 121 Running Total and Statistics

11 141 Time, Appointments, and Date Arithmetic

12 153 The Equation Solver

14 190 Additional Examples

More About Calculations

Assistance, Batteries, Memory, and Service

RPN The Stack

Menu Maps RPN Summary

RPN Selected Examples Error Messages Index

List of Examples

List of Examples

General Business Calculations

Currency Exchange Calculations

Interest Rate Conversions

How to Use the Equation Solver

Time, Alarms, and Date Arithmetic

Bonds and Notes

Running Total and Statistical Calculations

Important Information

Important Information

Adjusting the Display Contrast

Power On and Off Continuous Memory

Getting Started

Getting Started

What You See in the Display

Setting the Language

Keys for language Key Description

18 1 Getting Started

Backspacing and Clearing

Shift Key @

Keys for Clearing

Keys Display Description

20 1 Getting Started

Keys DisplayDescription

Doing Arithmetic

Using the Menu Keys

Keying in Negative Numbers

22 1 Getting Started

Menu Labels Menu Keys

Main Menu

24 1 Getting Started

Main Menu Menu Label Operations Done Covered This Category

Choosing Menus and Reading Menu Maps

Using the MU%C menu

26 1 Getting Started

Displaying the MU%C menu

Calculations Using Menus

Exiting Menus e

Clearing Values in Menus

28 1 Getting Started

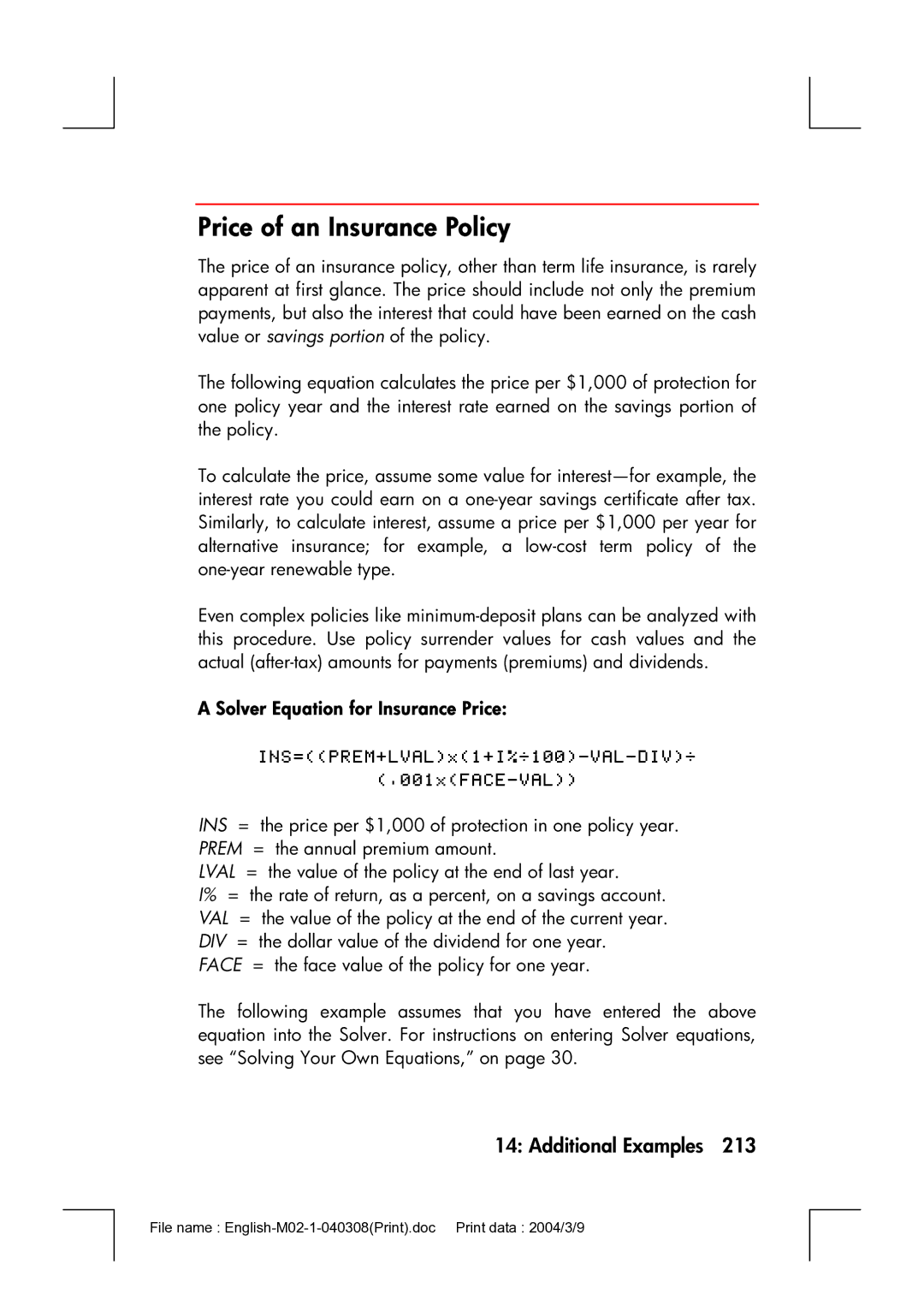

= Cost

Solving Your Own Equations Solve

30 1 Getting Started

Typing Words and Characters the ALPHAbetic Menu

Keys

Editing ALPHAbetic Text

Characters

Alphabetic Editing Operation Label or Key to Press

Calculating the Answer Calc

Keyboard

32 1 Getting Started

KeysDisplayDescription

Decimal Places

Controlling the Display Format

Internal Precision

Temporarily SHOWing ALL

Exchanging Periods and Commas in Numbers

Rounding a Number

Modes

Error Messages

36 1 Getting Started

Double Space. Press

Number of bytes Percentage of total Memory still free

Calculator Memory @M

Calculator Line

Arithmetic

VDoing Calculations

38 2 Arithmetic

VUsing Parentheses in Calculations

Keys Display

Arithmetic

VThe Percent Key

Mathematical Functions

40 2 Arithmetic

VThe Power Function Exponentiation

Shifted Math Functions

Key

Math Menu Labels

Math Menu

42 2 Arithmetic

Description

History Stack of Numbers

Saving and Reusing Numbers

VReusing the Last Result @L

VKeys Display

44 2 Arithmetic

VKeys Display Description

Storing and Recalling Numbers

Keys New Register Contents

Doing Arithmetic Inside Registers and Variables

Arithmetic in Registers

Scientific Notation

48 2 Arithmetic

Range of Numbers

Business Percentages BUS Menus Description

Percentage Calculations Business

Examples Using the BUS Menus

Using the BUS Menus

Percent Change %CHG

50 3 Percentage Calculations in Business

Percent of Total %TOTL

Markup as a Percent of Cost MU%C

Markup as a Percent of Price MU%P

52 3 Percentage Calculations in Business

Sharing Variables Between Menus

Currency Exchange Calculations

Currx Menu

54 4 Currency Exchange Calculation

Currx Menu

Selecting a Set of Currencies

Currency Exchange Calculation

Menu Key

Currencies

Entering a Rate

United States Conversion Chart in US$

Currency Rate

Select CAN$ as currency

Select HK$ as currency

58 4 Currency Exchange Calculation

Converting Between Two Currencies

Storing and Recalling Sets of Currencies

Example Converting between Hong Kong and U.S Dollars

60 4 Currency Exchange Calculation

Clearing the Currency Variables

Time Value of Money

TVM Menu

Time Value of Money

Second Level of TVM

First Level of TVM

First Level

TVM Menu Labels

Second Level

Shortcut for N Multiplies the number in the display by

64 5 Time Value of Money

Cash Flow Diagrams and Signs of Numbers

FV is

66 5 Time Value of Money

Using the TVM Menu

Loan Calculations

Figures and stores number

68 5 Time Value of Money

@c

Figures and stores

70 5 Time Value of Money

000

Savings Calculations

72 5 Time Value of Money

Figures and stores number

74 5 Time Value of Money

Leasing Calculations

76 5 Time Value of Money

Amortization Amrt

Amrt Menu Labels

Displaying an Amortization Schedule

Label

78 5 Time Value of Money

Time Value of Money

Next successive set of payments authorized

80 5 Time Value of Money

First year

82 5 Time Value of Money

Printing an Amortization Table Table

Calculates and prints

84 6 Interest Rate Conversions

Interest Rate Conversions

Icnv Menu

Converting Interest Rates

Interest Rate Conversions

86 6 Interest Rate Conversions

Compounding Periods Different from Payment Periods

88 6 Interest Rate Conversions

90 6 Interest Rate Conversions

Cash Flow Calculations

Cflo menu

Cash Flow Calculations

92 7 Cash Flow Calculations

Cflo Menu Labels

Cash Flows Ungrouped

94 7 Cash Flow Calculations

Creating a Cash-Flow List

For grouped cash flows The display now shows

Entering Cash Flows

96 7 Cash Flow Calculations

Prompting for #TIMES #T?. When the calculator displays

Display Description

Viewing and Correcting the List

Naming and Renaming a Cash-Flow List

Copying a Number from a List to the Calculator Line

98 7 Cash Flow Calculations

Deleting Cash Flows from List. Pressing

Clearing a Cash-Flow List and Its Name

Starting or GETting Another List

Viewing the Name of the Current List. Press , then e

100 7 Cash Flow Calculations

Cash-Flow Calculations IRR, NPV, NUS, NFV

Calc Menu for Cflo Lists Menu Label

102 7 Cash Flow Calculations

Calculates NPV

104 7 Cash Flow Calculations

Group Number Amount

Prompts for next cash

106 7 Cash Flow Calculations

Doing Other Calculations with Cflo Data

Bonds

Bond Menu

108 8 Bonds

Bond Menu Labels

Menu Description Label

Bonds

Doing Bond Calculations

110 8 Bonds

To calculate the price or yield of a bond

Since there is no call on

112 8 Bonds

MM.DDYYYY format

Depreciation

Deprc Menu

114 9 Depreciation

Depreciation

Deprc Menu Labels

DB, SOYD, and SL Methods

Doing Depreciation Calculations

116 9 Depreciation

To calculate the depreciation for an asset

Basis Salv 4,000

Acrs Method

Year Percentage Deductible Keys Display Description

118 9 Depreciation

Partial-Year Depreciation

120 9 Depreciation

Calendar Year Depreciation Value

Running Total and Statistics

Running Total and Statistics

SUM Menu

SUM Menu Labels

122 10 Running Total and Statistics

Entering Numbers and Viewing the Total

Creating a SUM List

124 10 Running Total and Statistics

Date

Amount Date

Transaction

126 10 Running Total and Statistics

Naming and Renaming a SUM List

Doing Statistical Calculations Calc

Clearing a SUM List and Its Name

Calculations with One Variable

Calc Menu for SUM Lists Menu Key

128 10 Running Total and Statistics

Expense

Month Phone

130 10 Running Total and Statistics

Calculations with Two Variables Frcst

Calc Total Mean Medn Stdev Range More MIN MAX Sort Frcst

132 10 Running Total and Statistics

Frcst Menu Labels

Logarithmic Curve Fit

Curve Fitting and Forecasting

To do curve fitting and forecasting

134 10 Running Total and Statistics

Number of Minutes Dollar Sales

Radio

Advertising Values

Minutes

136 10 Running Total and Statistics

Minutes

138 10 Running Total and Statistics

Weighted Mean and Grouped Standard Deviation

Rent

Summation Statistics

140 10 Running Total and Statistics

Doing Other Calculations with SUM Data

Time, Appointments, Date Arithmetic

Viewing the Time and Date

Time, Appointments, and Date Arithmetic

Time Menu

Time Menu Labels

142 11 Time, Appointments, and Date Arithmetic

SET Menu Labels

Setting the Time and Date SET

Menu Label Description

Or DD.MMYYYY

Adjusting the Clock Setting Adjst

Changing the Time and Date Formats SET

144 11 Time, Appointments, and Date Arithmetic

Viewing or Setting an Appointment APT1-APT10

Menu Labels for Setting Appointments Description

Appointments Appt

146 11 Time, Appointments, and Date Arithmetic

To set an appointment or view its current setting

Acknowledging an Appointment

Clearing Appointments

Unacknowledged Appointments

148 11 Time, Appointments, and Date Arithmetic

To acknowledge a past-due appointment

Date Arithmetic Calc

Calculating the Number of Days between Dates

Determining the Day of the Week for Any Date

Calc Menu Labels for Date Arithmetic

150 11 Time, Appointments, and Date Arithmetic

Calculating Past or Future Dates

DATE2

152 11 Time, Appointments, and Date Arithmetic

Equation Solver

Solver Example Sales Forecasts

Equation Solver

Next =OLD

154 12 The Equation Solver

Menu Label

Solve Menu

156 12 The Equation Solver

Keys

Entering Equations

Solve Menu Labels

To make an entry into the Solver list

Calculating Using Solver Menus Calc

To do a calculation using a Solver menu

158 12 The Equation Solver

Rmenu label

Eqty

160 12 The Equation Solver

Naming an Equation

Editing an Equation Edit

Shared Variables

Finding an Equation in the Solver List

Clearing Variables

162 12 The Equation Solver

Deleting a variable is quite different from clearing it

Deleting Variables and Equations

Deleting One Equation or Its Variables Delet

Writing Equations

Deleting All Equations or All Variables in the Solver @c

164 12 The Equation Solver

100

⋅ C

⋅ E

What Can Appear in an Equation

166 12 The Equation Solver

+ 5 ⋅ E

Using the Alpha Menu

Using a Typing Aid

Solver Functions

168 12 The Equation Solver

DDAYSd1d2cal

Solver Functions for Equations Description

HH.MMSS format

170 12 The Equation Solver

IFcond expr 1 expr

Svariable name

SIZECCFLO-listname

Cfr c 1 c 2 s expr

SIZESSUM-listname

#TCFLO-listnameflow#

172 12 The Equation Solver

Days

Conditional Expressions with if

OperatorKeys

≥ = ≤ = ≠ 174 12 The Equation Solver

Examples of Conditional Equations

Rating

VALUE=FIRST+1 ⎟ FIRST. If FIRST=0, then VALUE=FIRST

Percent Salary Increase

176 12 The Equation Solver

Summation Function ∑

Accessing Cflo and SUM Lists from the Solver

178 12 The Equation Solver

Creating Menus for Multiple Equations S Function

How the Solver Works

180 12 The Equation Solver

Halting and Restarting the Iterative Search

Entering Guesses

182 12 The Equation Solver

184 13 Printing

Printing

Double-Space Printing

Printer’s Power Source

Printing the DisplayP

Printing

Printing Variables, Lists, and Appointments List

Printing Other Information @p

Printer Menu Labels

186 13 Printing

Printing Descriptive Messages MSG

Trace Printing Trace

188 13 Printing

Keys Print-out

How to Interrupt the Printer

Loans

Additional Examples

Simple Annual Interest

190 14 Additional Examples

Additional Examples

Yield of a Discounted or Premium Mortgage

Figures and stores total

192 14 Additional Examples

See appendix F for RPN keystrokes for the next two examples

Annual Percentage Rate for a Loan with Fees

194 14 Additional Examples

11.5

Loan with an Odd Partial First Period

@c e

Solver Equation for Odd-Period Calculations

196 14 Additional Examples

Canadian Mortgages

Solver Equation for Canadian Mortgages

198 14 Additional Examples

Solver Equation for Advance Payments

Advance Payments Leasing

Savings

Value of a Fund with Regular Withdrawals

200 14 Additional Examples

Displays periodic

202 14 Additional Examples

Deposits Needed for a Child’s College Account

Additional Examples

204 14 Additional Examples

Flow of Withdrawals

For FLOW1

206 14 Additional Examples

Value of a Tax-Free Account

35

208 14 Additional Examples

Value of a Taxable Retirement Account

Modified Internal Rate of Return

Group No. of Months Cash Flow, $ Flow no

210 14 Additional Examples

V8 /12

180000

FLOW0

200000 I

V13 /12

212 14 Additional Examples

Solver Equation for Insurance Price

Price of an Insurance Policy

214 14 Additional Examples

Bonds

216 14 Additional Examples

Discounted Notes

Moving Average

Statistics

Solver Equation for Moving Averages

218 14 Additional Examples

Chi-Squared χ2 Statistics

Use

If necessary

If the expected values vary

220 14 Additional Examples

Number

Keystroke Display Description

Assistance, Batteries, Memory, and Service

Assistance, Batteries Memory, and Service

Answers to Common Questions

Obtaining Help in Operating the Calculator

Assistance, Batteries, Memory, and Service

Power and Batteries

Low-Power Indications

Do not use rechargeable batteries

Installing Batteries

Assistance, Batteries, Memory, and Service

Managing Calculator Memory

Reset hole

Resetting the Calculator

Erasing Continuous Memory

For English language

For the other languages

Clock Accuracy

Determining If the Calculator Requires Service

Environmental Limits

„ If the calculator won’t turn on

Assistance, Batteries, Memory, and Service

Confirming Calculator Operation Self-Test

Warranty

Assistance, Batteries, Memory, and Service

Europe Country Telephone numbers

Service

Asia Pacific Country Telephone numbers

America Country Telephone numbers

HP Invent

Regulatory information

Canada

Japan

IRR% Calculations

More About Calculations

Possible Outcomes of Calculating IRR%

More About Calculations

Storing a Guess for IRR%

Halting and Restarting the IRR% Calculation

Solver Calculations

Direct Solutions

O F I T = P R I C E - C O S T

S T = P R I C E - P R O F I T

= a R E a ⎟ W

E a = L x W

Iterative Solutions

More About Calculations

More About Calculations

More About Calculations

Actuarial Functions

Equations Used by Built-in Menus

Percentage Calculations in Business BUS

Time Value of Money TVM

Amortization

Cash-Flow Calculations

Interest Rate Conversions

NOM % P

NPV = CF0 + ∑CFj x Uspv i% nj x Sppv i% Nj

NUS = Uspv i% N Total = ∑nj ⋅ CFj

Bond Calculations

DB = Basis ⋅ Fact % /100

Depreciation Calculations

Sum and Statistics

Forecasting

Model Transformation

SXY = Σ X

Equations Used in Chapter

− M

SX 2 ⋅ SY

Odd-Period Calculations

Advance Payments

Modified Internal Rate of Return

Menu Maps

Menu Maps

Figure C-2. Currx Menu

Figure C-3. FIN Menu

Figure C-3 . FIN Menu

Figure C-4. SUM Menu

Figure C-5. Time Menu

Figure C-6. Solve Menu

About RPN

RPN Summary

About RPN on the hp 17bII+

RPN Summary

To select RPN mode Press @

Setting RPN Mode

Function Definition Key to Use Name

Where the RPN Functions Are

~ same as

Same as

Doing Calculations in RPN

Arithmetic Topics Affected by RPN Mode

Simple Arithmetic

↓. Except in Cflo and SUM lists, Efunction and the key also

To Calculate Press Display

27 %

RPN Mode ALG Mode

Calculations with STO and RCL

Chain Calculations-No Parentheses

Display

To Calculate Press

RPN The Stack

What the Stack Is

RPN The Stack

Exchanging the X- and Y-Registers in the Stack

Reviewing the Stack Roll Down

Arithmetic-How the Stack Does It

Lost

How Enter Works

Clearing Numbers

Reusing Numbers

Last X Register

Retrieving Numbers from Last

Chain Calculations

Exercises

Solution 23 @w13 E9 *-7@t+

RPN Selected Examples

RPN Selected Examples

KeysDisplay

Calculates annual interest

#TIMES1 for FLOW1

For E, press =, not

I11 I

Annual payment deposit

Error Messages

Error Messages

Error Messages

Error Messages

Error Messages

Index

Special Characters

Index

147

169

166

156

,

174-76

31-32

145

149

144

116

162-64

229

181-83

Examples

133

138-39

168-71

72-73

,

213-15

239

, 132 , 109 , 49, 53 , 52, 128 , 128 , 128 , 128

242-46

143-44

Memory. See also Continuous Memory

92-94

, 101 , 101 , 101 , 157 , 56 , 56 , 56 , 42

175

164-67

, 56 , 42 , 18 @p, 186 P

PMT. See also Payments in TVM, 63 rounded amortization

Repeating appointments past-due, 148 setting

Using

128

146-47

176

243-46

171

178

148

133-34

This regulation applies only to The Netherlands