HP 10bII+ Financial Calculator User’s Guide

HP Part Number NW239-90001 Edition 1, May

Legal Notice

HP 10bII+ Financial Calculator

Keyboard Map Legend

Number

Table of Contents

Page

Page

III

Basics of Key Functions

JGD

At a Glance

Shift Keys

Boxed Key Functions

Percentages

Jj7V1

JV§4

Add 15% to

DDÃ

JVÀ

GG¼

Memory Keys

J7GV

GG4

GV4

JYÏ

JG\Í

DSÙ

Time Value of Money TVM

TVM What if

JyÌ

D7VÒ

How much can you borrow at a 9.5% interest rate?

Amortize the 1 st through 24 th loan payments

Jæjg

Amortization

Depreciation

Interest Rate Conversion

\½\«

Cash Flows, IRR/YR, NPV, and NFV

JÆG¤

Yy¤

Yj¤

GD¤

Date and Calendar

G7GgGJ

VG4

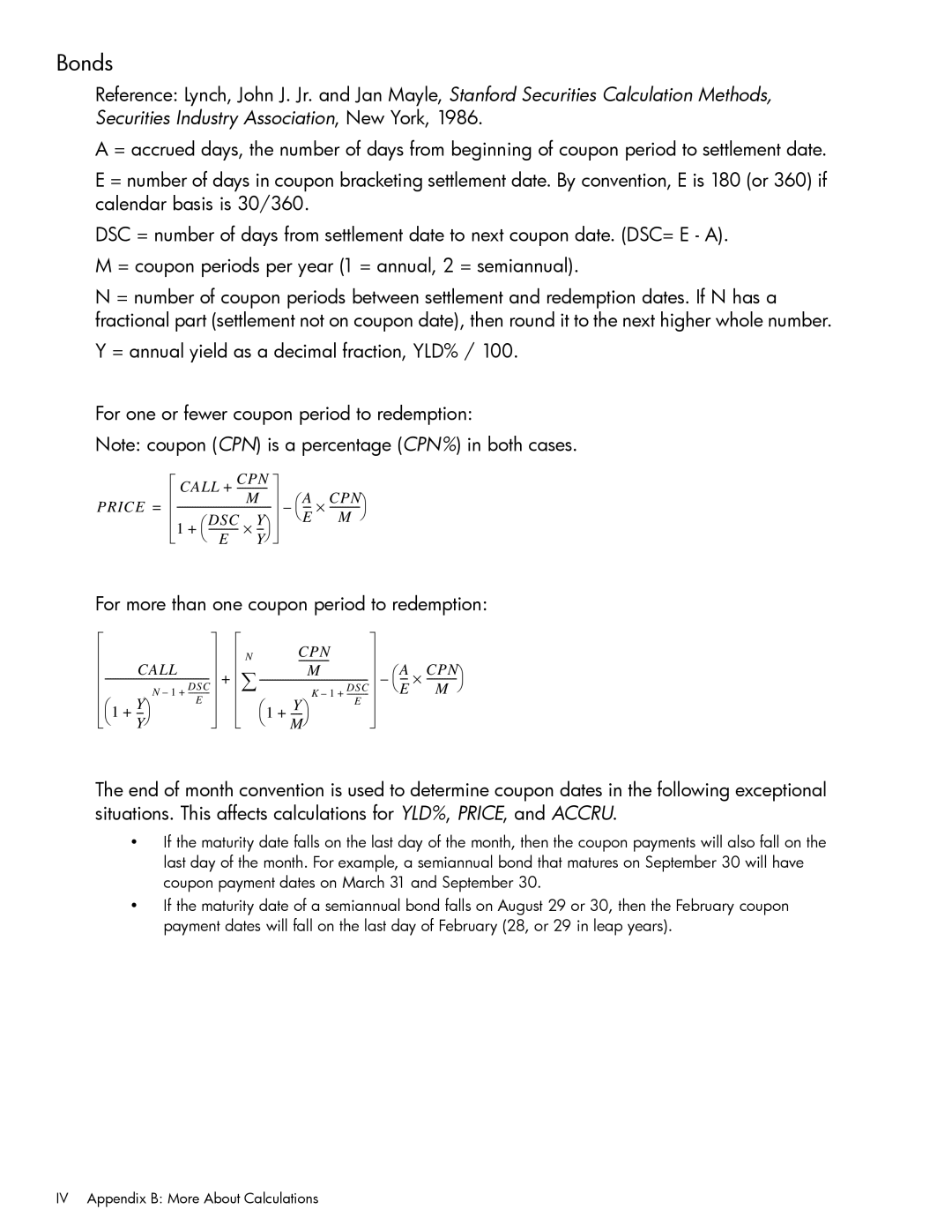

Bonds

For more information on bond calculations, refer to , Bonds

S7jVÎ

Y7jVÔ

Break-even

\h \«

\k \«

\T \«

\e \«

SÆJS¡

GÆV¡

YÆd¡

\T\«

17GV4

\5V

7VF

Probability

Find Sin θ =.62 in degrees. If RAD is displayed, press

7SG

Trigonometric Functions

Convert the results to radians using Pi

\aJg

At a Glance

Manual Conventions and Examples

Power On and Off

Getting Started

Displayed text

Item before the / is the alternate

Shift Keys

Simple Arithmetic Calculations

GY7jJ1SG7Yj4

JdPJG7Sg4

Operating Modes

S7dPV7DVa

Calculations in Chain Mode

1JJV7V4

7dJ4

Da\qgVA

Calculations in Algebraic Mode

Using Parentheses in Calculations

JG\n

Understanding the Display and Keyboard Cursor

JVy

AD4

Clearing the Calculator

Clearing Messages

Annunciators

Clear All

INV

Statistics Keys

Input Key

Swap Key

Same as pressing

Math Functions

Gd7GV\B

D7Vj1G7DS\b

One-Number Functions

Getting Started

J1SC

\5Y

JVc

7DVoR

YP\

A7SGoR

\5G

PY7V\2

Two-Number Functions

J7GVrc

17VdrC

In-line Functions

Gd\¨

Jj\¨

JjÆ

Gd1DD

Arithmetic with One-and Two-number Functions

-23below lists the two-number functions of the calculator

G7V\K

JGV\QD4

GG1JY\¨

VAJ7GV4

\Qv4

Last Answer

7JGVS4

\5D

YV7SP

Specifying Displayed Decimal Places

\zyJG

Jaj4

\54

D7gjSVYD

Messages

Business Percentage Keys

GV§

Business Percentages

Percent key

DJS7g4

JGV1j§

GdJ7j\¨

Jgpvæ

Margin and Markup Calculations

Gvvà

JdÀ

Margin Calculations

JVÃ

Using Margin and Markup Together

D7SÀ

V1Gª

Using Stored Numbers in Calculations

Using Constants

Number Storage and Storage Register Arithmetic

Example Calculate 10 + 10%, 11 + 10%, and 25 + 10%

J1J§ª

\QDª

Example Calculate 23

YV4

Using the M Register

VV\¨DGª

JY7GVm

Using Numbered Registers

Jjs

JS7dVm

VS7J1

YjV7S

\w7Y ADd7JV \wG

V7Y

\wPD

YV7j \wD

G7V

Picturing Financial Problems

How to approach a Financial Problem

Simple and Compound Interest

Signs of Cash Flows

Periods and Cash Flows

Simple Interest

Interest Rates

Compound Interest

Two Types of Financial Problems

Recognizing a TVM Problem

Recognizing a Cash Flow Problem

Cash flow diagram Borrower’s perspective

Cash flow diagram Investment in a mutual fund

TVM Keys

Using the TVM Application

Time Value of Money Calculations

Begin and End Modes

Loan Calculations

Jyva

Dpjgù

J7VÒ

JVÏ

1JV4

1VÌ

DjVyÌ

1JG4

J7VÒ

DDyÌ

G7gÒ

GV\Ú

JjGVÏ

Savings Calculations

YgÙ

1vÌ4

GyÏ

J7GÒ

GY\Í

GyÌ

YyÏ

S7DÒ

JV\Ú

Cash flow diagram Calculate the monthly lease payment

Lease Calculations

Cash flow diagram Calculate PV of the lease

JVÉ

1vÌy4

YjÙ

GYyÌ

Step Find the present value of the buy option

Step Add the results of ’ ’ and ’ ’

JVyÉ

1p4

To Amortize

Amort key on the HP 10bII+ allows you to calculate

J7jVÒ

Jygvï

Jdægy

JJ7VÒ

Amortize the 1st, 25th, and 54th payments

GVÆ

VYÆ

Investments With Different Compounding Periods

S7j\Ó

Interest Rate Conversions

First Bank

DS\Í

S7SV\Ó

S7SD\Ó

Compounding and Payment Periods Differ

DSV\Í

GVyÌ

Resetting the TVM Keys

Depreciation

Depreciation Keys

Item in the selected format

Inputs 5 for the expected useful life

Depreciation example using Declining Balance Keys

How to Use the Cash Flow Application

Cash Flow Calculations

Clearing the Cash Flow Memory

Number1 ¤

Cash Flow Calculations

Calculating Internal Rate of Return

Vy¤

Gy¤

NPV and IRR/YR Discounting Cash Flows

JJjSV7Gd¤

AJG

Organizing Cash Flows

JJy¤

Initial cash flow and cash flow groups

Viewing and Editing Cash Flows

11GÆ

Calculating Net Present Value and Net Future Value

JVÆ1GÆ

1JGyÆ1G

VÆG¤

ÆY¤

VÆJ¤

JÆJ¤

JVÆJ¤

Æd¤

JVÒ

Cash flow diagram Calculates NPV

Automatic Storage of IRR/YR and NPV

Date Format

Calendar Formats and Date Calculations

Calendar Format

Using the Input key

Date Calculations and Number of Days

Date Calculation

\ÇJ4

To enter the data for this example using the Ækey

JG7JgGJJ

ÆJ\Ç

DJ7JGJ4

\5S

Y7SGJ\Ä

J7JjGJG

S7YGJV\Ä

Using the Ækey

J7JjGJGÆ

Bonds

Bond Keys

Y7GgGJ

JYË

S7YGG

V7VÎ

JJÑ

Y7JVGJG

Resetting the bond keys

J7JVGG

Break-even

Break-even Keys

Break-even example

Calculating the projected maximum fixed cost

Resetting the Break-even keys

\e\«

\k\«

\h\«

\Z\«

Clearing Statistical Data

Entering Statistical Data

Two-Variable Statistics and Weighted Mean

One-Variable Statistics

Viewing and Editing Statistical Data

YD\W\5G

DGÆYJV¡

DVÆVJV¡

YV\W

YDÆJGD¡

DjÆSgV¡

Summary of Statistical Calculations

D7V¡

Y7V¡

D7GV¡

D7jV¡

JjjÆgD¡

JdDÆd¡

JgGÆgJ¡

JgVÆjj¡

400

DÆJJ¡ VÆGGSV¡

GÆJY¡

JÆdG¡

VÆGgd¡

Weighted Mean

VJÆgg¡

VÆVY¡

VVÆDG¡

VJSÆdG¡

Permutations

Probability Calculations

Factorial

V9D4

VD4

VÆD

VÆD9

YG\w6

Advanced Probability Distributions

J7jyF

Normal Lower Tail Probability

7GVoF

Inverse of Normal Lower Tail Probability

Students T Probability Lower Tail

GIJ7gSy4

GÆJ7gSyI

Inverse of Student’s t Probability Lower Tail

GSoI7V4

GSÆ7VoI

Y1J4

Conversions from Lower Tail

J7GyF

PG4

Returns desired value of z

Statistical Calculations

Additional Examples

Setting a Sales Price

\qJ1\q GaJ4

Business Applications

DÆJDS¡

JÆJ¡

GÆJJGJ¡

YÆJSjV¡ VÆGVd¡

\qDA

Gpdspj

\q\qJ AG\n

YVsPJ§

YVjG7gy

Jg§

AJPJ4

Yield of a Discounted or Premium Mortgage

G7VÒ

VÙAYGÙ

JdyÏ

Annual Percentage Rate for a Loan With Fees

JGÒ

JSÏ

AG§Ï

AD§Ï

YV\Ǥ4

AJGP

JSaDP

1YVÏ

PvÙ4

Jgvï

D7VÒ

Jjvï

ÉD\Ú

JG\Ó

JDÏ

Canadian Mortgages

What if … TVM Calculations

JJ7GÒ

DVVVyÌ

VÏ4

GS\Í

PvÙ1

Savings

Stores effective rate as annual

Jyyù

Gains That Go Untaxed Until Withdrawal

Yòìï

DVÙ

PJV§4

Cash Flow Examples

G7JjVAGg

DyÌ

Wrap-Around Mortgages

Cash flow diagram Wrap-around mortgage

GGVJ7GG

GG\¥

DVy¤

VÌyAjVY

VÌy¤

Installing Batteries

Power and Batteries

Low Power Annunciator

Appendix a Batteries and Answers to Common Questions

Calculator won’t turn on

Determining if the Calculator Requires Service

Resetting the calculator

Erasing the calculator’s memory

See Determining If the Calculator Requires Service

Answers to Common Questions

Environmental Limits

Equations

Appendix B More About Calculations

IRR/YR Calculations

Amortization

Payment Mode Factor S = 0 for End mode 1 for Begin mode

Time Value of Money TVM

Interest Rate Conversions

Cash-Flow Calculations

Bonds

For more than one coupon period to redemption

Depreciation

Statistics

Forecasting

Cashflow memory was cleared

Appendix C Messages

Memory has been erased Ch

Tvm registers were cleared

Bond registers were cleared

Statistical memory and registers were cleared

Limited Hardware Warranty Period

Warranty, Regulatory, and Contact Information

HP Limited Hardware Warranty and Customer Care

Replacing the Batteries

General Terms

Exclusions

Modifications

European Union Regulatory Notice

Canadian Notice

Avis Canadien

Germany

Perchlorate Material special handling may apply

Customer Care Contact Information

香港特別行

ไทย

Tobago Tunisia Turkey Türkiye Turks 01-800-711-2884

Warranty, Regulatory, and Contact Information

Warranty, Regulatory, and Contact Information

Chain mode

Advance payments Algebraic mode

Battery

Error messages Factorial

Keyboard

In-line functions Interest

Interest rate conversions Investments

Keys

Modes

Trigonometric functions Troubleshooting

Warranty

Operating modes Parentheses