• |

|

|

|

|

|

|

| = | S |

| + | 1 | T |

| ||

|

|

|

|

|

|

|

|

| t + 1 | t | t | |||||

|

|

|

| S1S3 | – S22 | |

|

|

|

| α |

| ||||

c = exp |

| 1 | |

|

|

|

|

|

|

|

|

| ||||

+ S3 |

|

|

|

|

|

|

|

|

| |||||||

|

| n | S1 | – 2S2 |

|

|

|

|

|

|

|

|

| |||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||

a | = exp |

| (b – 1)(S2 – S1) | |

| ||||

2 | ||||

|

|

| b(bn – 1) | |

|

|

|

| |

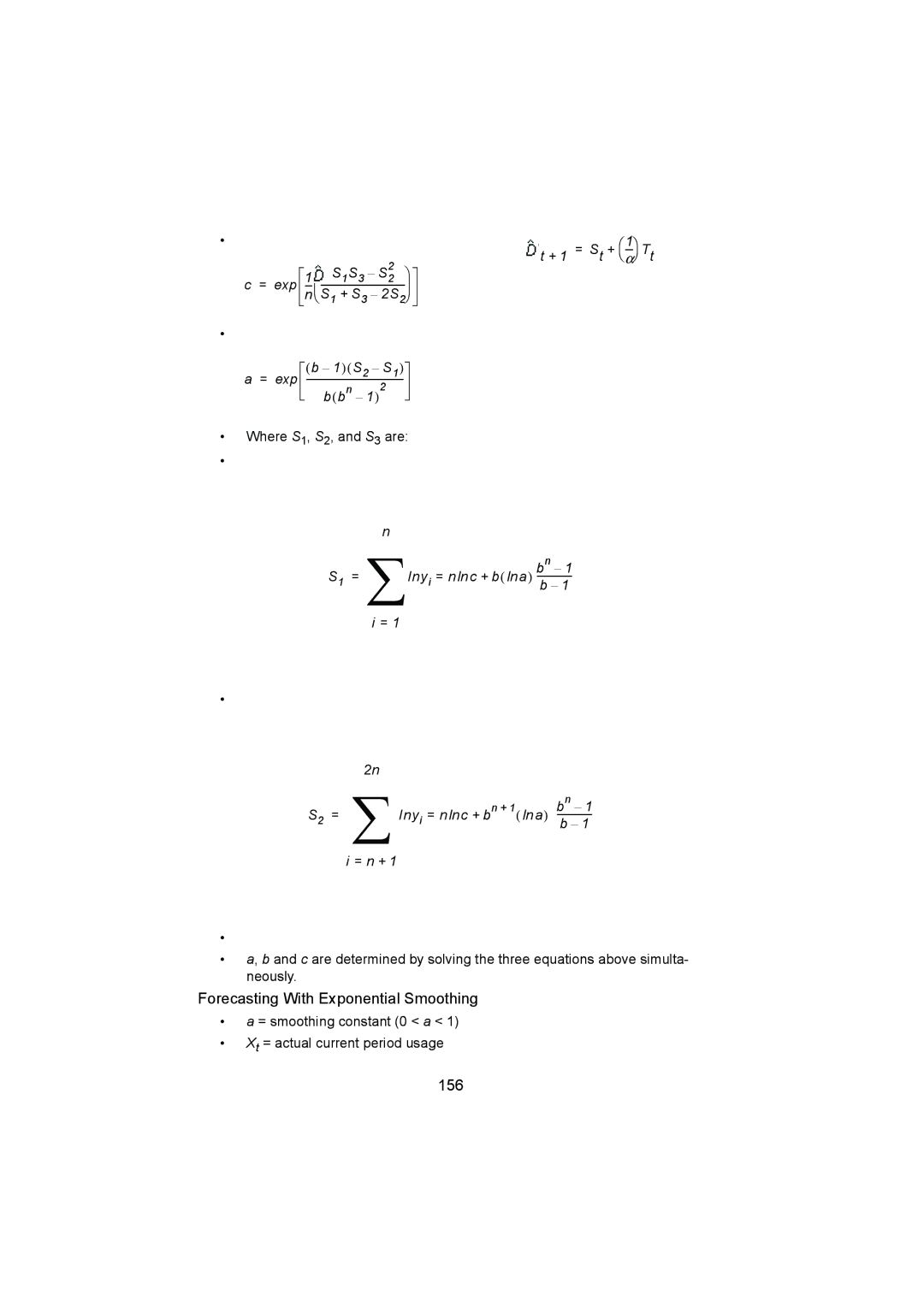

•Where S1, S2, and S3 are:

n

S1 = ∑Inyi = n lnc +

i = 1

•

2n

bn – 1 b( lna)

b – 1

S |

| = | ∑ | Iny |

| = n lnc + b | n + 1 | ( lna) | bn | – 1 |

2 | i |

| ||||||||

|

|

|

|

|

| b | – 1 | |||

i = n + 1

•

•a, b and c are determined by solving the three equations above simulta- neously.

Forecasting With Exponential Smoothing

•a = smoothing constant (0 < a < 1)

•Xt = actual current period usage